What is digital banking? Digital banking means delivering banking services online. Apart from providing access to a number of services available at brick-and-mortar banks, digital banking is a safe and dynamic way to help customers manage their budgets and receive assistance with financial questions. Modern digital banking solutions combine security best practices, smooth user experiences, and smart loyalty programs to give users what they want at their fingertips.

Research by American Bankers Association reveals that over 50 percent of Americans are conducting banking via mobile apps. And we can understand them. Mobile banking development services are maturing and becoming sophisticated, with more innovative and practical solutions appearing on the market. This is encouraging more people to use mobile banking solutions each year as well as increasing the number of mobile banking application development companies on the market. According to Statista, more than 79 percent of the US population will be using digital banking services by the end of 2029.

The development of mobile banking and implementation of digital banking functionality has a number of advantages both for traditional offline banks rethinking their operating models and new market players building their digital presence from scratch. In this article, we overview popular digital banking development services and discuss mobile banking app development on your own. We also cover different types of software development in bank applications and examples of neobank bank development.

Who’s using digital banking and why?

Banking software solutions and financial software development services emerged in response to global digitalization and now there is almost no person left who doesn’t know what is a digital bank. However, going digital is still just a goal for many banking institutions. Research by Cornerstone Advisors revealed that 27 percent of banks were only planning to launch a digital transformation strategy in 2021. With this in mind, you can conclude that launching your digital banking solution now puts you one step ahead of those who are still considering mobile banking development services.

Before you start, here are a few things you’ll want to know about digital banking users.

Target audience for banking software solutions

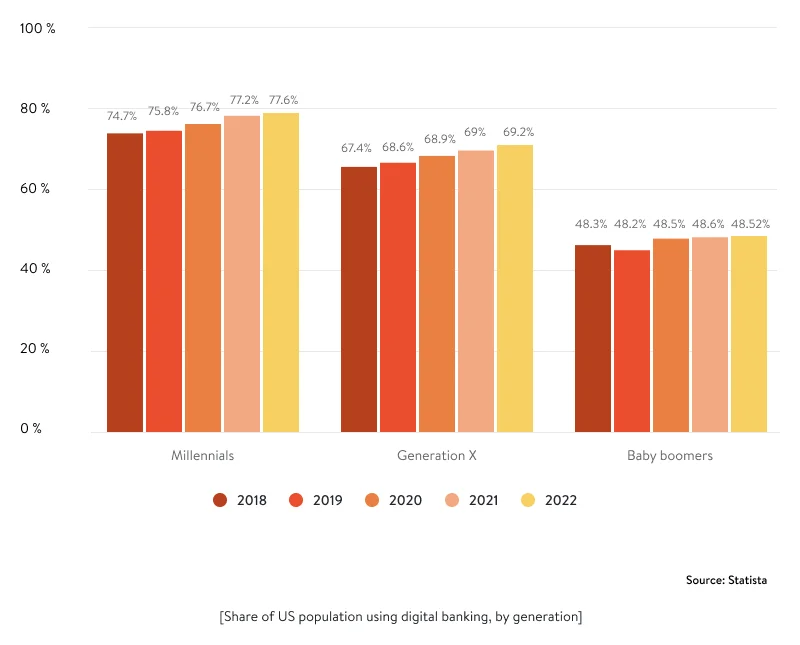

Digital transformation is traditionally associated with Millennials, who are considered its creators and the main driving force behind it.

As the statistics show, representatives of Generation X and Baby Boomers are using digital banking less than Millenials, though their share is still rather high.

But for the changes COVID-19 has brought, we could stop here and conclude that in your digital banking development you should primarily target Millennials and younger generations. During the coronavirus pandemic, however, those who used to prefer face-to-face communication had to learn a new way of interaction when brick-and-mortar bank offices imposed pandemic-related restrictions. With online banking suddenly becoming a safer way to handle financial matters, more people started using it. For example, iResearch Services reveals that 90 percent of people over the age of 60 used online banking for the first time during the pandemic.

When thinking about the users you’d like to target with your mobile banking app, we recommend taking into account the needs of different age groups. Along with that, you should consider the demand for online banking services and address users’ key expectations.

What do users expect from mobile banking product development?

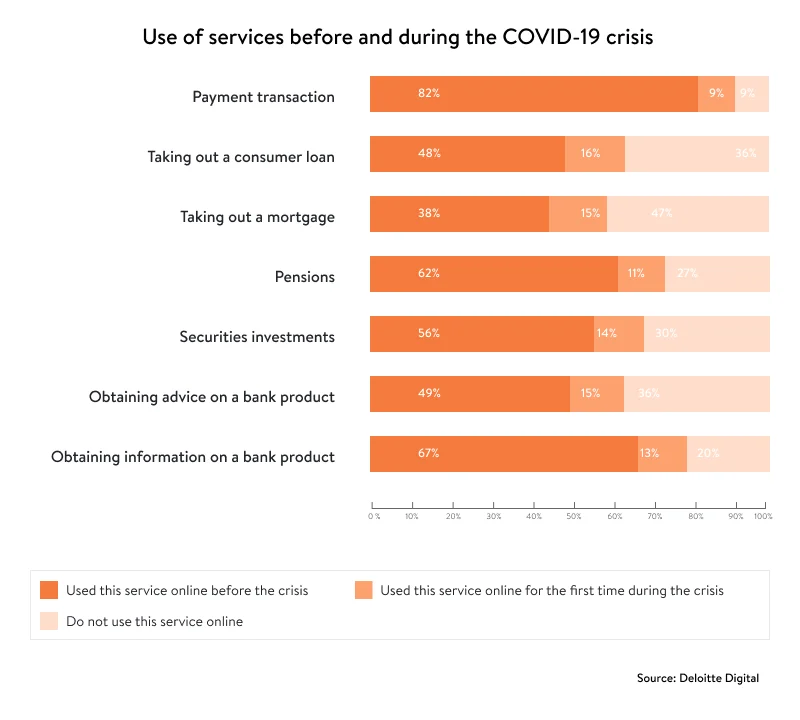

In their “Digital banking redefined in 2021” report, Deloitte Digital explores the demand for mobile banking before and during the pandemic. According to Deloitte, Americans mostly used digital banking for payment transactions (82 percent), obtaining information on a bank product (67 percent), and getting pensions (62 percent) in 2019.

Things completely changed in 2020 and 2021. Recent research by Deloitte focused on exploring what banking services users tried for the first time during the pandemic. The results showed that during the pandemic 33% of Americans took out a consumer loan through online banking for the first time, 29% took out mortgages in the same manner, and 25% invested in securities electronically for the first time.

The above data clearly shows that digital banking is gaining momentum and shows no signs of stopping. Today, when interacting with a mobile bank, users expect transparency, a smooth experience, and security. But before diving into ways to achieve these, let’s have a look at digital banking solutions that have been on the market for a while to learn from them.

Overview of the digital banking market

The term “digital banking” is broad. Among modern digital banking solutions, we can distinguish three types of banking software:

- Online banking software is a way for conventional banks to deliver features and services via a customer profile on the website,

- Mobile banking refers to dedicated software that allows customers to access banking features via mobile devices.

- Neobanking software is a type of digital banking app that appeared as a way to challenge traditional banks by providing services without any physical branches. Neobanks are a real trend in the FinTech industry. Statista estimates there will be 39.1 million US neobank account holders in 2025. Well-known neobanks include Chime, Varo Bank, Monzo, and Revolut.

Now let’s overview some of the digital banking solutions we’ve mentioned and learn how they paved their way to success.

Popular banking software solutions

Many successful banking service providers were originally launched as startups. Before long, the quality of services they delivered to customers along with the diverse functionality available in their apps helped them gain the trust of customers and extensive funding from investors.

Chime calls itself “a banking app built by a tech company.” This FinTech giant was founded in 2013 in San Francisco as an alternative to traditional banking. Thanks to innovative ideas and extensive funding the company acquired to implement them, today Chime offers a number of services including secure transactions, automated savings, fee-free overdrafts, credit history builder. Chime customers can withdraw cash at more than 60,000 fee-free ATMs located at popular stores. Having been installed 6.4 million times in just half a year, the Chime app became the most downloaded digital banking software in the US in 2021.

Revolut is a European digital-only bank headquartered in London. With 150 million monthly transactions and more than 15 million users, Revolut became the most valuable FinTech company in the UK in July 2021. Apart from supporting spending and ATM withdrawals in 120 currencies and transfers in 29 currencies directly from the app, Revolut offers low exchange fees and provides extensive crypto and stock trading capabilities. So far, Revolut services are available in 28 European countries. The company has also applied for a bank charter in the US.

Monzo is a UK-based neobank founded in 2015 that did a soft launch in the US in 2020. But in 2021, after unsuccessful attempts to get a US banking license, Monzo withdrew their application, announcing they would continue searching for new routes to enter and compete with other players on the local market. Monzo’s major features include organizing budgets, earning interest on savings, and sending money abroad with no fees or extra charges. The bank also provides favorable fee-free options for international money transfers, letting users hold and exchange 29 currencies. Statista estimates the Monzo app will have more than nine million downloads on iOS and Android in 2022, making Monzo the second most popular digital banking app in the UK after Revolut.

N26 is a German neobank that operates in 24 European countries. Launched as a startup, N26 took three years to acquire a banking license. Until they did, the bank operated using an interface over a backend provided by Wirecard, a German payment processor and financial services provider. In 2019, N26 soft launched in the United States and partnered with Axos Bank to issue Visa cards for US customers, but in January 2022 N26 discontinued US operations to focus on their European business. This digital banking solution allows users to set up direct deposits, perform international money transfers, and track spending. It also has a cashback system available in the app.

Ally Bank is a full-service online bank operated by Ally Financial Inc., a US bank holding company. Ally was launched as a separate FinTech product in 2009. In 2013, the company first introduced a mobile app for iPad, and a year after they announced the launch of the app on Android and Kindle Fire tablets. When in 2015 Ally found out that half of their retail deposit customers were using online banking, they introduced a redesigned online banking experience which contributed to the way Ally Bank provides digital services today. As of 2021, Ally achieved 85 percent customer satisfaction.

So many different stories stand behind the success of the world’s top banking software solutions. There is definitely much to learn from them. Let’s figure out what it takes to create your own digital banking app.

How to create a mobile banking app and a top-notch digital banking platform

In today’s competitive market, financial software development for digital banking requires a holistic approach. Along with equipping your software with must-have features, we recommend looking at competitors and carefully exploring your target audience to create a product they will love.

Must-have features to build a banking app

The basic functionality of modern digital banking apps is far more diverse than the functionality of banking apps just a couple of years ago. Users expect banking software to be useful in budget planning, provide real-time support with financial questions, offer investment and trading opportunities, point to the nearest ATM, and make it easy to take out a loan. Along with that, they strive to keep banking details private and money safe. So what are the must-have features of modern banking apps?

- Secure login and authorization

- Account management

- Money transfer

- Digital payments

- Expense tracking

- Mobile check deposit

- A cashback system

- Notifications

- An ATM locator

- In-app customer support

The advanced functionality of modern digital banking solutions include:

- Virtual cards

- Integration with digital wallet services

- Invoicing

The list of supplementary features can go on, and it does, as the demand for quality mobile banking app development services as well as their diversity keeps growing each day. At the same time, a step-by-step approach to feature implementation helps to create a product tailored to users’ essential needs and enrich it with more functionality when needed.

Mobile banking software development challenges

Creating banking software solutions entails challenges that you and your mobile banking app development company need to overcome to make a great product and deliver it to consumers. Before you actually set out to write app requirements and develop the app architecture, there are various steps you should take.

Now let’s get down to listing the challenges of mobile-only banking app development at all stages, from ideation to realization.

Applying for a banking license

Acquiring a banking license is the first large obstacle that digital banks face when they decide to create a mobile app. In the EU, banking licenses are issued by local financial regulators such as central banks or market supervisors, which are called National Competent Authorities (NCAs). If you need a US banking license, you’ll need to go through the Office of the Controller of the Currency (OCC) to obtain a Federal Charter. Both in the EU and the US, to obtain a banking license you’ll be required to provide your business plan and detailed information on shareholders, your director, and officers. A banking license obliges a digital bank to request approval from the license holder each time they plan to release a new feature or adjust a digital banking strategy.

Once the application is submitted, what follows is a chain of checks that legal authorities initiate to make sure you comply with requirements such as the minimum number of directors and shareholders’ places of residence.

Additionally, you’ll have to comply with security requirements to pass the Payment Card Industry Data Security Standard (PCI DSS) audit and prove that your organization takes measures to prevent payment data breaches and card fraud. Depending on the number of transactions your organization handles each year, you’ll fall into one of the four PCI compliance levels. Ensuring the security of your banking software is definitely a topic for discussion, which is why we’ll cover it in more detail in the next section.

There are more requirements you’ll need to comply with throughout the development process. For example, if you decide to implement any crypto or trading functionality, you’ll need to acquire a broker license or set up an integration with a dedicated broker and get a license to be able to display information from the broker in your digital banking app.

Complying with industry requirements

Apart from the PCI DSS requirements that apply to organizations globally, there are laws, standards, and regulations introduced by local authorities.

- The General Data Protection Regulation (GDPR) is an EU regulation that describes a set of rules for personal data protection.

- The New Payment Services Directive (PSD2) introduces security requirements for the initiation and processing of electronic payments and sets standards for consumer protections across the EU and European Economic Area (EEA).

- Local laws and regulations. These are legal requirements issued by regional authorities, such as states. An example is the California Consumer Privacy Act (CCPA), a California state statute that intends to enhance privacy rights and consumer protections for residents of California, giving them more control over the personal information businesses collect.

Creating a smooth user experience

A good mobile banking app combines functionality aimed at solving users’ issues with a smooth user experience (UX). Taking into account the diverse audience for digital banking software, it’s crucial to provide each age group with comprehensive digital assets to onboard and use your app.

Nowadays, neobanks apply a design thinking approach, which means designing products and services exactly in the way end users expect. In other words, design thinking is based on actually communicating with users instead of building hypotheses about their needs and expectations.

Increasing product LTV and attracting new customers

In terms of FinTech development, LTV, or lifetime value, refers to the revenue provided by bank users throughout the whole period of their interaction with the bank. To generate a stable revenue flow, a digital bank needs to provide its customers with convenient conditions for working with and spending their funds. This can be achieved, for example, by allowing customers to add a credit card to a digital wallet or by introducing personal electronic credentials for secure identification and signing (such as a BankID).

At some point in development, you’ll be searching for ways to attract more customers to your banking software. If the quality of service is good and the user experience is smooth, your customers will likely be talking about your app. To enhance your reputation, make sure your app is rated highly on the App Store and Google Play Store and tackle a low frequency for PPC if it exists. If it isn’t, think of improving your customer service and listening to what people are not satisfied with. For one of our projects, we created an in-app questionnaire for digital bank customers to see which in-app events customers liked and which they didn’t. If a user said they liked an event, we asked them to rate the app on the app store. Otherwise, the user was redirected to get help from the support team. This helped us achieve a high rating on both app stores.

What else defines the success of your online banking software development?

Carefully choosing tech stack for digital banking, ensuring enhanced security measures, creating a smooth user experience, and thinking of smart ways to reach out to a broader audience are the key points of payment app development.

One more thing that contributes to the success of your banking app is choosing the right software development provider. Here are some principles to keep in mind during the mobile banking app development process.

- Forming expectations is critical for both the product owner and the development team. Understanding expectations helps you avoid an expectation gap and builds mutual credibility.

- Overall transparency throughout the development process allows you to match expectations with reality and gives you full control over your technical team.

- Your team’s initiative and proactivity will open more opportunities for product development and scaling.

- Thinking ahead and knowing the market will help your team make decisions aimed at growing your business and, in the long-term perspective, save on marketing efforts.

- A creative approach combined with technical expertise. Modern digital banking software has gained the trust of audiences by combining the right technology stack for banking applications with amazing features and user experiences that make people’s lives easier and create a wow effect.

- Reliable project management is a must if you aim to get a fully functional software product with your time frame and budget.

When working on projects in the FinTech domain, we recommend starting with a proof of concept (PoC). Let’s give an example to illustrate how this approach applies to developing a digital banking app. Say you aim to increase the data processing speed so that a request reaches a third-party service in less than one second – this way, you’ll always have the most recent data.

Our team understands that this is a priority for you and starts creating a relevant hypothesis. To prove the hypothesis, we create a bare app interface and set up integrations with third-party services in a way that satisfies your requirements. This allows us to understand which way to go to keep your priorities. At the same time, developing a PoC helps you and your stakeholders invest money in something that works instead of developing a full-fledged system from scratch with no real guarantees about its capacity and capabilities.

Searching for a reliable development partner to create a digital bank?

We’re here to help

FAQ

How to build a mobile banking app

Study your competition and the target audience. Implement must-have functionality like account management, digital payments, and money transfer. Keep in mind that building mobile banking solutions entails challenges including acquiring a banking license, complying with industry requirements, and providing a smooth user experience. In this article, we discuss the required features and how to solve the above-mentioned challenges.

How can you choose a mobile banking app development company?

You can find a software development partner for creating your banking solution on digital business directories like Clutch and GoodFirms. Having picked the profile of the firm you think suits best your needs, go to its website, explore the reviews and ratings, and view the completed projects. Keep in mind that partnering with an established company rather than individual freelancers provides more guarantees and decreases risks.

Why opt for our digital banking development services?

We are experienced in building custom banking solutions including ERP banking systems, customer portals, and mobile and web banking apps. We have an established approach to end-to-end financial software development. Thanks to our contribution, our clients experienced significant growth in the customer base, customer engagement improvement, and customer attrition reduction.

About the author